There is no denying that the US economy is booming – the rate of people seeking unemployment benefits has dropped to its lowest since 1969, and there are more job openings than people looking for work. But while a decrease in unemployment is an overall positive experience, there are downsides. For example, finding qualified employees for available positions has become increasingly difficult. However, more job openings could also be a sign that businesses are expanding exponentially, which could be an excellent sign for business survival rates in the US.

Are companies simply getting bigger, or are startups continuously sprouting and sticking around? We collected data from the US Bureau of Labor Statistics Establishment Age and Survival report to see how long businesses typically operate, which industries close the fastest, and where businesses are expanding. Keep reading to see what we found.

How long businesses survive

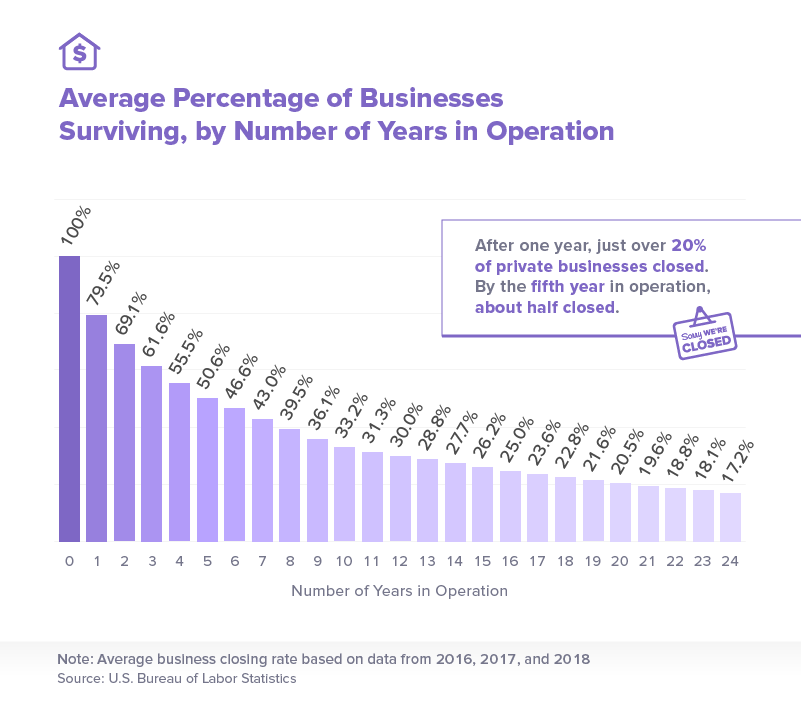

The business world is risky, and no matter how qualified or prepared someone is, there is no guarantee of immediate or lasting success. In fact, only 80% of private businesses will remain in operation after the first year. The number of businesses open will steadily dwindle from there, with only about half remaining by the fifth year. And by year 20, a little over 20% of businesses will still operate, ultimately reaching a low of 17.2% by the 24th year.

While a lack of experience and issues bringing in capital are sure to bring down a business, they are not the only reasons that startups fail. For some businesses, there simply might not be a market for what is offered. Customers are the foundation of success for small businesses, and if they don’t need or want the product being sold, the business can be at risk of closing. Additionally, competition, pricing, and not having the right team can cause a new business to fail. It may also just be a case of bad luck.

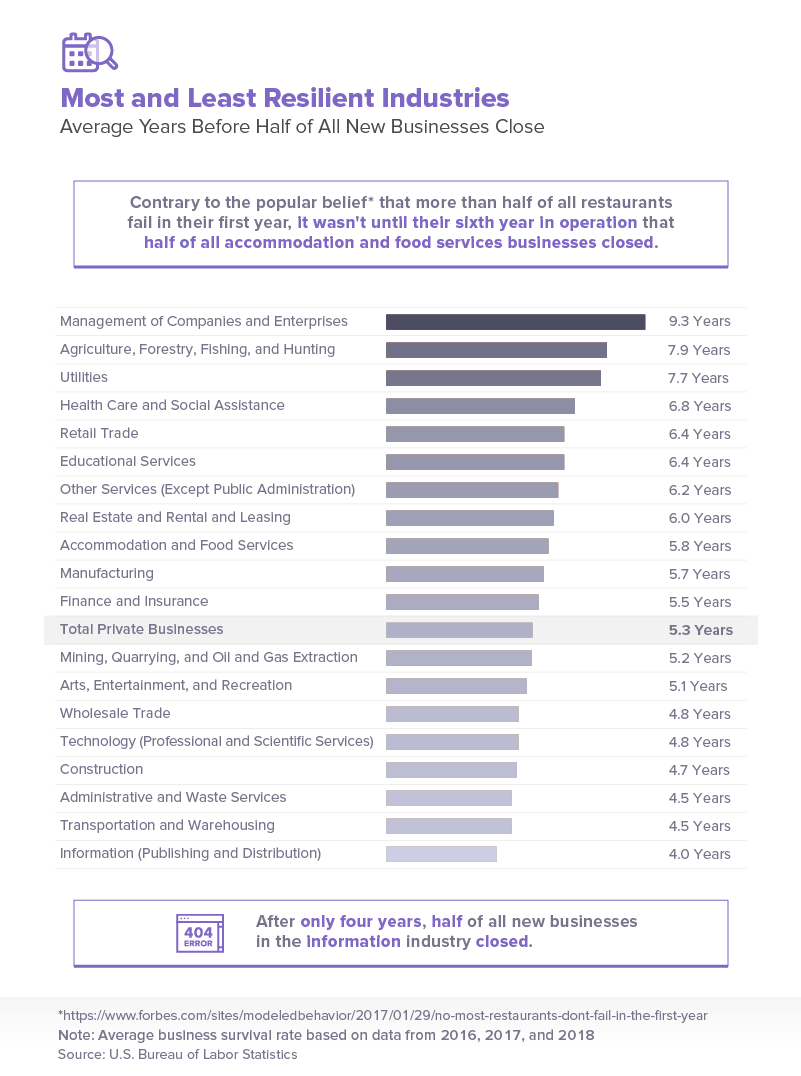

The industries with the best business survival rates

Half of all businesses may close around five years, but certain industries are significantly more resilient than others. The management of companies and enterprises industry was, by far, the most resilient, with 9.3 years passing before half of its new businesses closed. The agriculture, forestry, fishing, and hunting industry, along with utilities, also had some of the longest life spans, with half of the new businesses closing after 7.9 and 7.7 years, respectively.

Despite the claim that most restaurants close their doors in the first year of business, it wasn’t until the sixth year that half of all new businesses in the accommodation and food services industry closed, according to BLS data. On the other hand, half of the businesses in the technology and construction industry closed after just 4.8 and 4.7 years, respectively – despite both industries ranking in the top 10 industries with the most growth and profit.

The least resilient industry, however, was information, with half of all information businesses closing after four years in operation. While the information industry covers a wide array of fields, the shift to online platforms may hurt new businesses, with media companies feeling the backlash of the internet and the free content it brings.

The best states for new businesses

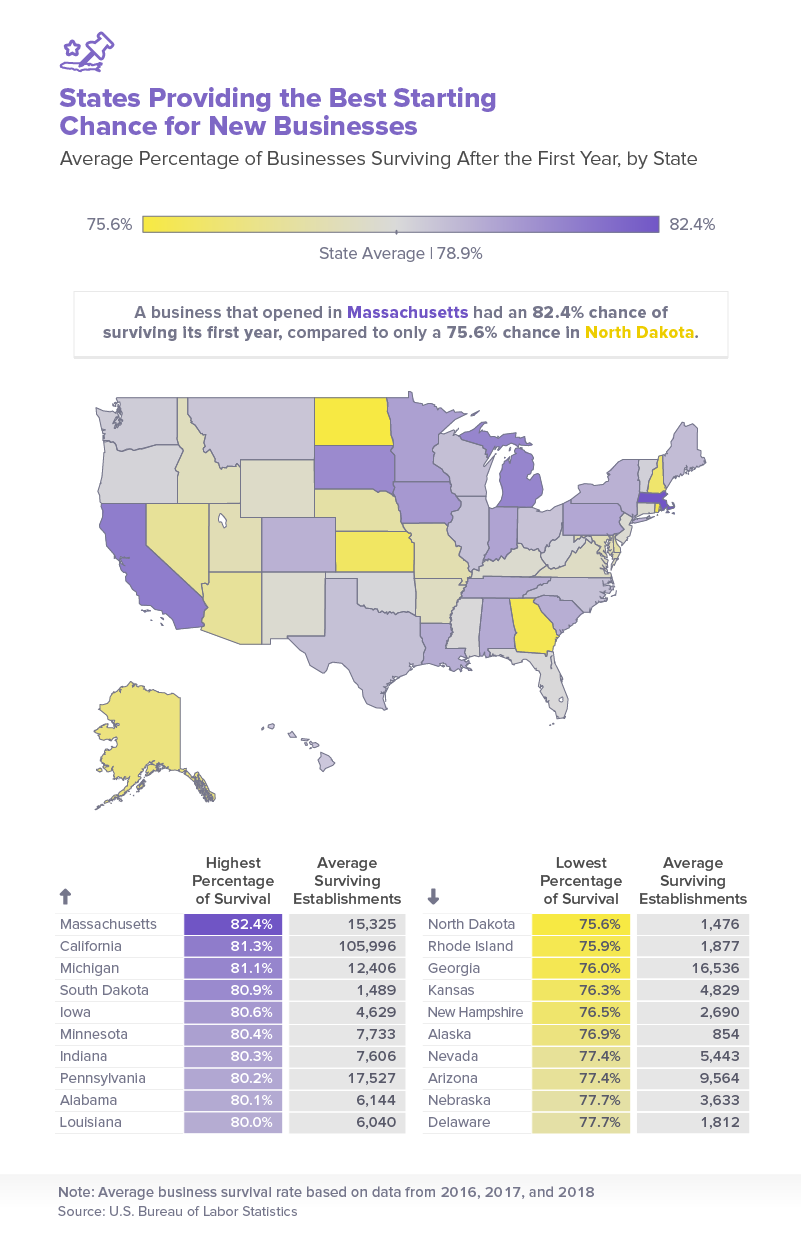

While people may be moving to Florida and California because business is booming and wages are rising, entrepreneurs may not fare as well in Florida. The Sunshine State ranked just above the national average, with 79% of new businesses surviving the first year, on average. On the other side of the country, however, 81.3% of new businesses in California made it past a year, making it the second-best state for a starting chance. The only state with better odds was Massachusetts, where an average of 82.4% of businesses survived. However, while California has a slightly lower percentage of survival, over 100,000 new businesses remained open between 2016 and 2018 – that’s over six times more businesses than Massachusetts.

New businesses in North Dakota, Rhode Island, and Georgia faced the greatest chance of failing, with each state having around a 76% chance of survival. However, each of these states has a substantial amount of startups. Between 2010 and 2015, North Dakota saw a spike in small business startups, while the most recent peak in Rhode Island and Georgia occurred in 2015. However, along with many businesses opening comes an increase in the number of companies ceasing operation.

Location may play a major role in determining a business’s success, but factors like talent, work ethic, sales, and even local laws and regulations can turn a good business idea into a closed shop. Learning how to navigate around obstacles and make proper use of resources can help any business survive – regardless of where it’s started.

The best states for resiliency

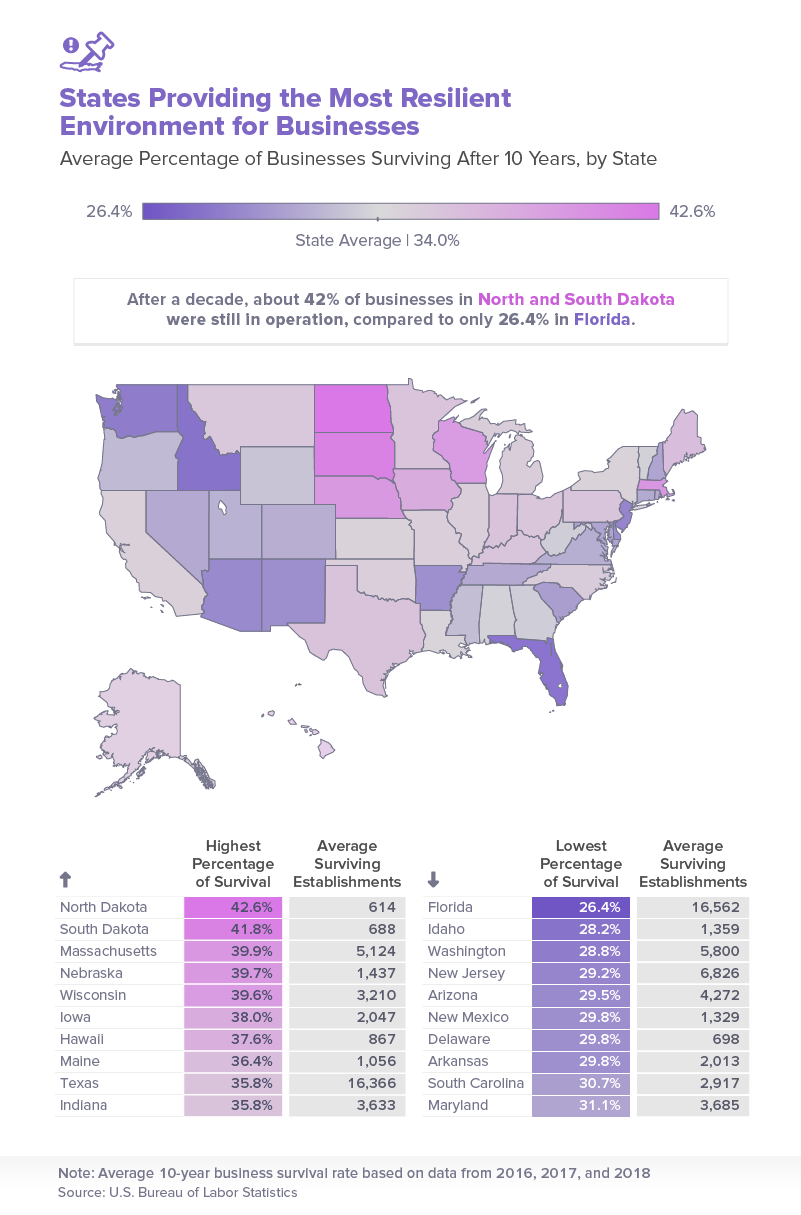

Making it past the first year of operation doesn’t necessarily mean long-term success. When looking at business survival after ten years, the state with the greatest chance of survival was also the state with the lowest likelihood of businesses making it past a year. This time, North Dakota topped the chart, with 42.6% of businesses remaining open after a decade. South Dakota wasn’t too far behind, with 41.8% of businesses surviving after ten years of operation.

On the other hand, Florida had the worst survival rate, with just 26.4% of businesses making it past a decade. The state’s ranking may not be a reflection of the economy, though. Rather, Florida’s susceptibility to hurricanes often forces businesses to close their doors permanently. Considering the majority of Florida’s population (and businesses) resides on the coasts, damage from natural disasters may prevent businesses from making it past the 10-year mark.

The best states for stability

Considering half of all businesses shut down by the time five years roll around, most would expect longevity to be a sign of success. Massachusetts was one of the states with the most stable timelines – the state ranked first for business survival after one year and five years and only dropped down to third by the 10th year. Vermont’s business survival rate also remained pretty steady, ranking 24th in the first year and just 27th by year 10.

However, Ohio, Utah, Alaska, Pennsylvania, and Nebraska were just a few states with more drastic changes over the years. While the states may have ranked high or low in their first year, survival rates typically assumed the opposite by five or ten years. One thing is for sure: First-year survival rates are not accurate predictors of overall business longevity.

North Dakota’s recent oil boom may explain the state’s extreme trajectory from having the worst first-year survival rate to the best 10-year rate. At its peak, the state boasted the lowest unemployment rate in the country. In 2014, the economy experienced a lull when oil prices collapsed, causing small towns and businesses to suffer. However, oil production has since ramped up.

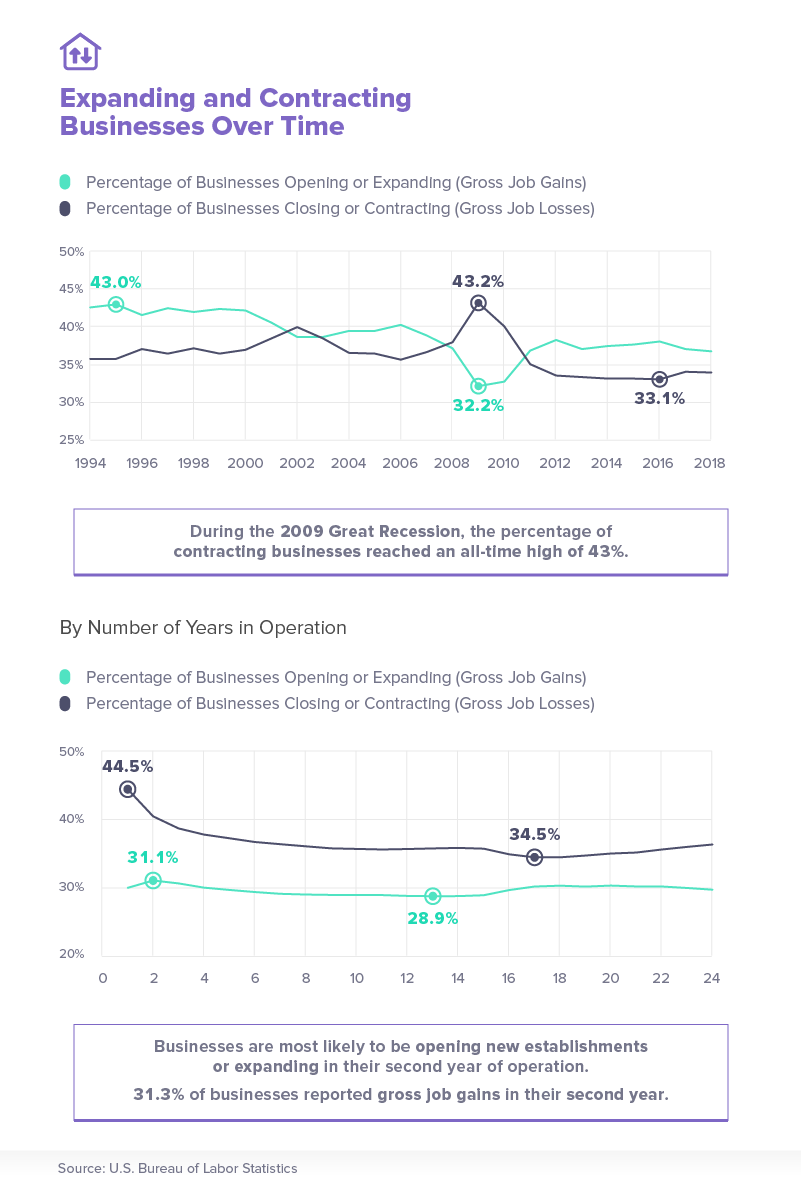

Gains over losses

If businesses are opening and subsequently closing, how is the job market flooded with position openings? One reason may be due to the expansion businesses undergo over time. Since the Great Recession in 2009, which caused 43% of businesses to close or contract, the percentage of businesses opening or expanding – and, therefore, increasing job gains – has been on a steady incline. Between 2017 and 2018, however, the gap between open and closed businesses shrank, with the percentage of businesses opening decreasing to 37% and the percentage of businesses closing increasing to 34%.

The closing and expansion rate of businesses remained slightly steadier over their time in operation. The first year saw the greatest number of closures, but by the second year, businesses saw the highest expansion, with just under a third growing their business. Another jump in expansion occurred after the 15th year of operation and remained elevated for at least the next ten years.

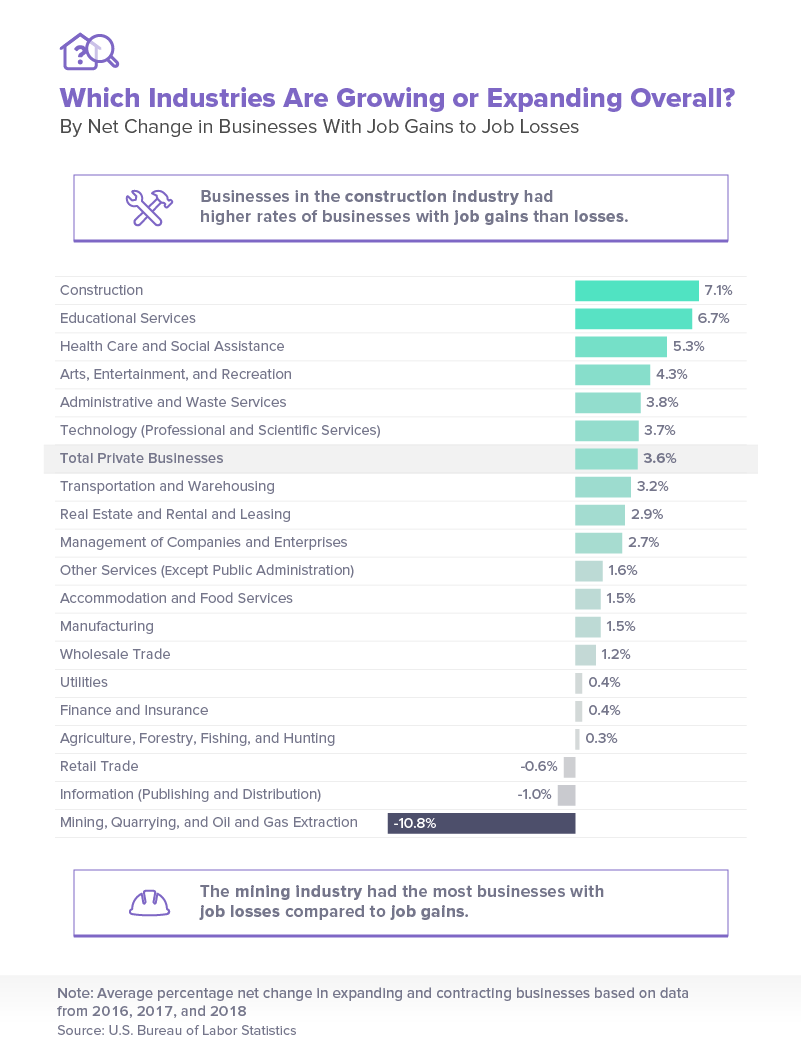

Industry expansion

The US has been on a record-long job growth streak, reaching over 100 consecutive months of increasing jobs. While this is a sign of a thriving economy, certain industries aren’t seeing the same growth as others. It’s likely no surprise that the technology industry is one of the fastest growing; however, in terms of job gains compared to losses, the construction industry topped the chart. Compared to 3.7 percent of businesses experiencing growth in the technology industry, 7.1% of businesses in the construction sector had more gains than losses.

While the majority of industries saw more gains than losses, the retail trade, information, and mining industries saw more losses than gains. In retail trade and information, though, the difference was slim – there were just 1% more losses than gains in the information industry, and 0.6% more losses than gains in retail. Mining, quarrying, and oil and gas extraction, on the other hand, had nearly 11% more losses than gains. The decline of the mining industry has occurred for years – since 2008, coal production and the number of mines have steadily declined, and coal mining jobs have declined right along with them. The mining industry may be in trouble of not surviving, but with renewable energy taking the spotlight, it could all balance out.

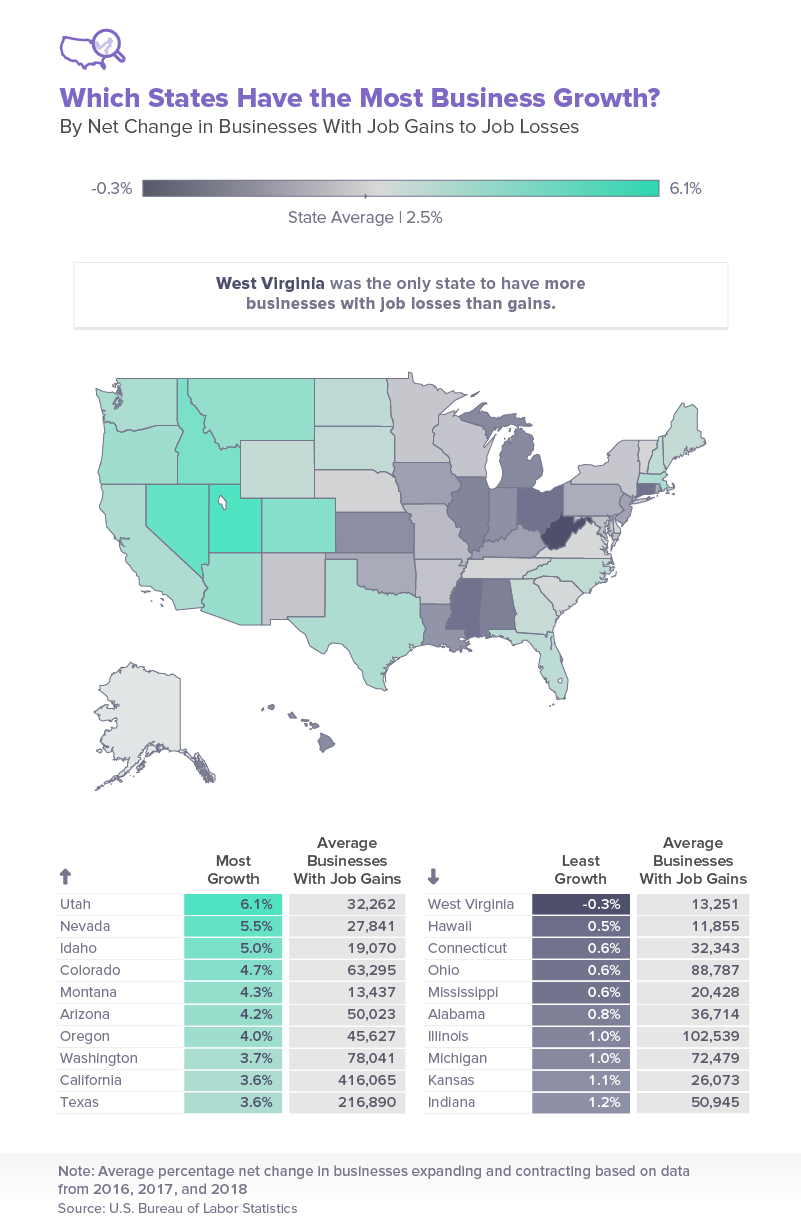

United States of growth

Just as industries vary in expansion and contraction, so too do states. Utah had the most growth with 6.1% more gains than losses. The state’s job growth, high labor force participation, and low unemployment rate earned it the top spot for employment. Nevada followed closely behind Utah with 5.5% more businesses growing than closing. However, California and Texas had significantly more businesses with job gains overall, despite a lower percentage than Utah and Nevada – even with just 3.6 percent of businesses seeing growth, California and Texas had an average of 416,065 and 216,890 businesses experiencing job gains, respectively.

While plenty of states had significantly less growth, only one state had more losses than gains – 0.3% more businesses contracted than grew in West Virginia. This decline in West Virginia’s businesses is likely related to its decreasing population and growing poverty rate. In 2018, the Mountain State lost over 11,000 residents, while its poverty rate increased from 17.9% to 19.1% in just a year.

Critical challenges that impact business survival

Embarking on a business venture is akin to navigating a complex maze, with success hinging on the ability to overcome multifaceted challenges. Understanding the factors that could potentially bring down a business is pivotal for entrepreneurs seeking longevity and prosperity in the competitive landscape.

1. Lack of Experience

In the entrepreneurial journey, experience is a formidable ally. Navigating the intricacies of business operations, industry nuances, and market dynamics requires seasoned insights. Lack of experience can lead to missteps in decision-making, strategy formulation, and overall business management.

2. Capital Challenges

Sufficient capital is the lifeblood of any business. Inadequate funding can stifle growth, limit operational capabilities, and impede the ability to weather unforeseen challenges. Businesses must navigate the delicate balance of securing initial capital, managing cash flow, and seeking sustainable sources of funding.

3. Market Demand

The heartbeat of a successful business is its alignment with market demand. Products or services that fail to resonate with the target audience face an uphill battle. Thorough market research, staying attuned to changing consumer preferences, and adapting offerings accordingly are crucial for sustained relevance.

4. Intense Competition

Thriving in a competitive landscape demands strategic prowess. Businesses grappling with fierce competition must differentiate themselves through innovation, superior quality, or exceptional service. Understanding competitors, identifying unique value propositions, and adapting swiftly are key elements of success.

5. Pricing Strategies

The delicate art of pricing can significantly impact a business’s viability. Overpricing may deter potential customers while underpricing could compromise profitability. Striking the right balance requires a nuanced understanding of market dynamics, perceived value, and competitive benchmarks.

6. Team Dynamics

A cohesive and skilled team is the backbone of business success. Discordant team dynamics, lack of effective communication, or a mismatch of skills can undermine operational efficiency. Fostering a positive work culture, promoting collaboration, and investing in team development contribute to a resilient workforce.

7. Lack of Adaptability

The business landscape is dynamic, and adaptability is a survival skill. Failing to adapt to emerging trends, technological advancements, or shifts in consumer behavior can render a business obsolete. Embracing change, continuous learning, and agility are essential for staying ahead of the curve.

8. Inadequate Marketing Strategies

Visibility in the marketplace is pivotal for attracting customers. Businesses relying on inadequate or ineffective marketing strategies may struggle to reach their target audience. A robust marketing plan, encompassing online and offline channels, is essential for brand awareness and customer acquisition.

9. Regulatory and Compliance Challenges

Navigating the regulatory landscape is integral to business sustainability. Failure to comply with industry regulations, tax obligations, or legal requirements can lead to fines, legal disputes, and reputational damage. Businesses must stay informed and ensure rigorous adherence to applicable laws.

10. External Economic Factors

The broader economic environment can exert significant influence. Businesses may face headwinds from economic downturns, geopolitical instability, or unforeseen global events. Diversifying risk, monitoring economic indicators, and implementing contingency plans enhance resilience.

11. Technological Obsolescence

In the era of rapid technological advancement, businesses relying on outdated technologies risk obsolescence. Embracing modern tools, staying abreast of technological trends, and fostering a culture of innovation are vital for staying competitive.

12. Poor Customer Relations

Customer satisfaction is the bedrock of brand loyalty. Businesses neglecting customer relations, providing subpar customer service, or overlooking feedback risk losing clientele. Prioritizing customer engagement, addressing concerns promptly, and cultivating positive relationships contribute to long-term success.

In the intricate tapestry of business challenges, recognizing these factors empowers entrepreneurs to proactively address and mitigate risks. By navigating these hurdles with resilience, adaptability, and strategic acumen, businesses can chart a course toward sustained growth and prosperity.

Business survival and teamwork

Numerous factors determine the survival of a business. Surviving the first year is only accomplished by 80% of businesses, and by the fifth year, half are no longer operating. But making it to the fifth year isn’t necessarily a sign of strength. By the 10th year in operation, some businesses are still forced to close their doors, especially in Florida.

Opening a business is clearly risky, so knowing which states and industries are the most resilient is vital to making the right move. But picking the location and type of business is only one part of the equation. Forming a qualified, cohesive team to back your business and provide employees with the proper tools can increase the chances of your business surviving. At Nulab, we are dedicated to providing businesses with the best software to facilitate efficient teamwork. To learn more about products that can help your team run smoothly, visit us online today.

Sources

https://www.cnbc.com/2018/06/05/there-are-more-jobs-than-people-out-of-work.html

https://www.cnbc.com/2018/10/16/top-10-industries-that-are-hiring-thriving-and-making-money.html

https://www.apnews.com/4c463558fb70464591b823ff5add3be7

https://www.cnbc.com/2019/04/26/us-cities-where-business-is-booming-and-salaries-are-rising.html

https://www.sba.gov/sites/default/files/advocacy/2018-Small-Business-Profiles-ND.pdf

https://www.sba.gov/sites/default/files/advocacy/2018-Small-Business-Profiles-RI.pdf

https://www.sba.gov/sites/default/files/advocacy/2018-Small-Business-Profiles-GA.pdf

https://www.entrepreneur.com/article/305688

https://www.inc.com/leigh-buchanan/why-local-regulations-are-increasing.html

http://worldpopulationreview.com/states/florida-population/

https://www.marketwatch.com/story/us-job-openings-jump-to-record-71-million-2018-10-16

https://www.cnbc.com/2018/08/23/trump-says-the-coal-industry-is-back-the-data-say-otherwise.html

https://www.usnews.com/news/best-states/rankings/economy/employment

https://www.cbsnews.com/news/west-virginia-poverty-gets-worse-under-trump-economy-not-better/

Methodology

We collected data from the US Bureau of Labor Statistics Establishment Age and Survival statistics. Data were downloaded on May 15, 2019. Our analysis included data from Table 4: “Number of private sector establishments by direction of employment change by establishment age, as a percentage of total establishments” and Table 7: “Survival of private sector establishments by opening year.”

The net change in businesses with job gains versus job losses was calculated by subtracting the percentage of establishments with gross job losses from the percentage of establishments with gross job gains. All data were limited to recent statistics from 2016 through 2018 unless shown annually over time.

Data are limited to private businesses.

Fair use statement

Luck may play a part in successful businesses, but being informed about the risks is the best way to increase the chance of survival. If you know someone who could benefit from the findings of our study, feel free to share it with them. The graphics and content of this project are available for noncommercial reuse. Just make sure to link back to this page to give the authors proper credit.

This post was originally published on August 5, 2019, and updated most recently on December 4, 2023.

About Author